You land a bigger project than your firm has ever signed. The team is excited. Then the operational mess starts.

The client wants a deposit now, revised milestone billing later, and a separate approval flow for reimbursable expenses. Your PM is tracking part of it in QuickBooks, part in spreadsheets, and part in email. Vendors want payment before the next phase starts. Your cash is tight even though your pipeline looks strong. On paper, you're growing. In practice, you're floating the work.

That gap is where most growing design firms get punished. Not because they lack demand. Because their financial systems still look like a small studio's back office while their project load looks like a mature firm's responsibility.

From Creative Passion to Financial Pressure

A lot of architecture and design founders hit the same wall. They built the firm through talent, taste, relationships, and relentless work. That model gets you the first wave of success. It doesn't automatically give you a payment system that can handle retainers, phase billing, change orders, product pass-throughs, or international clients.

The problem gets sharper because the market is expanding. The global product design and development services market was valued at USD 18,507.3 million in 2024 and is projected to reach USD 32,926.4 million by 2030, growing at a CAGR of 10.1%, according to Grand View Research's global market outlook. More opportunity sounds great. It also means more firms will compete on speed, polish, and operational reliability.

Growth exposes weak financial habits

Early on, you can get away with founder memory and manual follow-up. You know every client personally. You remember who pays late. You send invoices yourself. You absorb the friction.

That stops working when your firm starts juggling multiple jobs at different stages. One late payment can delay a consultant invoice. One sloppy scope can turn into unbilled work. One mismatched payment platform can force clients into awkward payment methods that slow everything down.

Practical rule: If your revenue is growing faster than your billing discipline, your stress will grow faster than your profit.

Merchant advisory matters here because this isn't just about card processing. It's about designing the financial operating system around how creative firms earn money. Deposits. Progress billing. Product sourcing. Approval delays. Variable project value. Client expectations that often belong to enterprise buyers, even when your internal systems don't.

Back office isn't the right label

Founders often treat billing and payment acceptance like administrative chores. That's a mistake. The way you collect money shapes your cash flow, your pricing confidence, your client experience, and your ability to hire ahead of demand.

If your invoicing process is clunky, clients notice. If your contracts don't match your billing logic, you weaken your position. If your payment tools can't support the way your projects unfold, your team starts working around the system instead of through it.

Merchant advisory for growing design firms fixes that by putting structure where growth usually creates chaos.

What Merchant Advisory Means for Your Design Firm

Merchant advisory for a design firm isn't a generic merchant account pitch. It's a strategic review of how your firm accepts money, invoices work, manages payment timing, reduces friction, and protects margin.

A generic provider will try to sell you a processor. A strong advisor will look at how your business operates. They ask better questions. Do you bill by phase or by retainer? Do you collect reimbursables separately? Do you pass through procurement costs? Do clients pay by ACH, card, wire, or portal? Are your terms aligned with your production schedule?

Think like a financial architect

Your firm already understands the value of intentional systems. You wouldn't let a complex building go from concept to construction without plans, sequencing, coordination, and quality control. Your financial infrastructure deserves the same discipline.

For a design business, merchant advisory should cover at least these areas:

- Payment acceptance design: Which payment methods you offer, when you offer them, and how those choices affect cost and client convenience.

- Billing workflow: How invoices are triggered, approved, formatted, and followed up.

- Cash flow timing: Whether your collections schedule matches your cost structure.

- Contract alignment: Whether your legal terms support the payment behavior you need.

- System integration: Whether your payment stack talks cleanly to tools like QuickBooks, Stripe, or your project management platform.

The need is real because creative service firms are often ignored in standard merchant content. An underserved issue in the $2.4 trillion global payments industry is the cost of payment acceptance for creative providers, especially around deposits, milestone payments, and international billing, as noted in McKinsey's analysis of guardrails for payments growth.

What this looks like in practice

A design-focused advisor helps you make decisions like these:

- Use ACH for large domestic invoices when the client relationship supports it.

- Reserve card acceptance for deposits or smaller balances where speed matters more than cost.

- Separate service invoices from pass-through expenses so clients understand what they're approving.

- Standardize milestone events so billing happens when work is completed, not when someone remembers.

- Build a client payment experience that feels premium, not improvised.

Good merchant advisory removes friction for the client and hidden leakage for the firm.

If you're still thinking of merchant services as a rates conversation, you're thinking too small. For a growing design firm, it's an operational design problem. Solve it well, and billing becomes a strength instead of a recurring source of drag.

The Five Financial Levers a Merchant Advisor Optimizes

Design firms carry unusual financial pressure. You influence large purchasing decisions, manage complex projects, and often shoulder production costs before the client's money arrives. In the U.S. design industry, the average designer's specification influence equals 40 times the buying power of a typical consumer, and top firms reach 140x, according to the 2025 U.S. Design Industry Benchmark Report from ThinkLab. That level of commercial influence deserves tighter financial controls than most firms currently have.

Payment acceptance

The first lever is simple. Stop accepting payments in ways that erode your margin.

Many firms default to whatever method the client prefers. That's generous and often expensive. A merchant advisor helps you build rules. Large invoice by ACH. Deposit by card if you want speed. International payment through a platform that reduces friction and keeps records clean. Wire only when necessary.

This isn't about being rigid. It's about using payment types intentionally instead of reactively.

Billing and invoicing

The second lever is your billing engine. Weak invoicing creates avoidable delay.

A strong setup defines who sends invoices, when they're triggered, what backup is attached, and how reminders are handled. It also cleans up presentation. Architecture and design clients often expect polished communication. A sloppy invoice undermines trust in a premium firm.

Use tools that reduce manual handling. QuickBooks can work. Stripe can work. The issue isn't brand loyalty. It's whether the workflow fits project billing.

Cash flow timing

Most growing firms don't have a revenue problem. They have a timing problem.

You may be profitable on paper while still struggling to cover payroll, consultants, software, travel, fabrication, or photography. That's why billing schedules should track real project effort and real cost exposure. Deposits need to be meaningful. Milestones need to happen before your biggest outlays, not after them.

If you routinely finance client work from your operating account, your terms are wrong.

Pricing discipline

The fourth lever is pricing. Merchant advisory should inform how you package and present fees, not just how you collect them.

Clients react differently to fixed fees, retainers, phase fees, procurement support, and reimbursables. Your payment structure can either reinforce value or blur it. If a client can't easily tell what they're paying for, they challenge invoices more often.

This is also where brand presentation matters. The way your work is documented and positioned influences how confidently clients accept premium pricing. Strong visual proof can support that value conversation. Firms that invest in clear presentation often see the business upside discussed in this piece on the ROI of professional photography.

Contract terms

The fifth lever is contract structure. Too many firms try to solve payment problems after the agreement is signed.

Your contracts should define deposit requirements, invoice timing, reimbursement treatment, late payment terms, scope expansion, suspension rights, and approval deadlines. If those points are vague, the client controls the pace. If they're clear, your team can enforce process without drama.

Here are the clauses worth tightening first:

- Deposit language: State the amount or method clearly and tie project kickoff to receipt.

- Milestone definitions: Use deliverables or project phases that both sides can recognize.

- Expense treatment: Clarify which costs are billed separately and when.

- Pause rights: Give your firm the right to stop work if payments stall.

- Approval windows: Keep feedback delays from becoming billing delays.

Merchant advisory earns its keep when these five levers work together. Better acceptance rules without better contracts won't fix your cash flow. Better invoices without pricing clarity won't stop disputes. This is a system, not a patch.

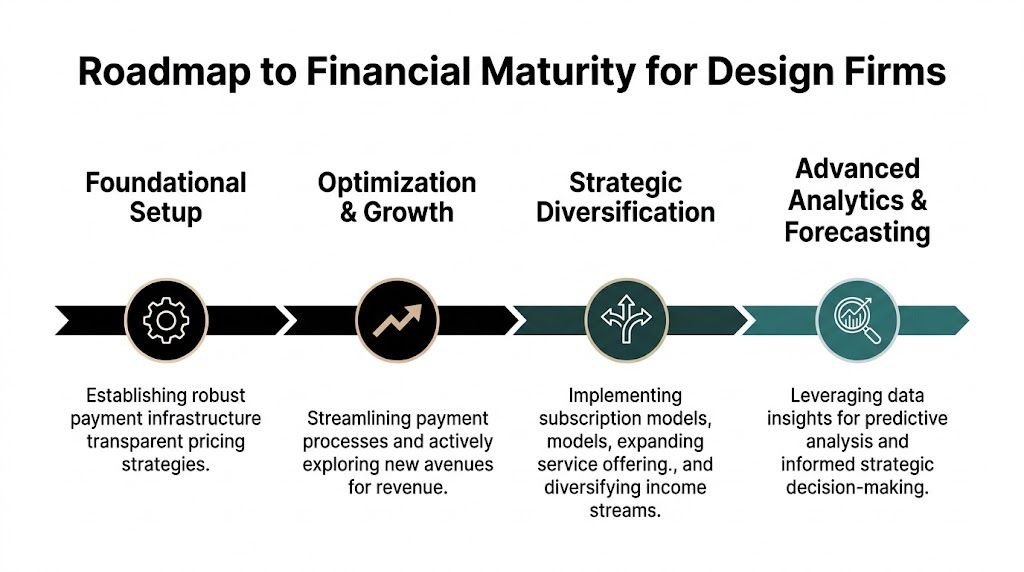

A Staged Roadmap to Financial Maturity

Most firms don't need a dramatic overhaul. They need a staged plan with accountability. That's how you move from founder-driven improvisation to a financial system that scales.

A structured roadmap matters because technical assistance programs help position entrepreneurs for capital access, and for design firms that means stronger financial operations can support the move from founder-led delivery to a model lenders or investors can evaluate, according to the Milken Institute report on best practices for technical assistance programs.

Phase one audit the current mess

Start with a diagnostic. Not a vague discussion. An actual review.

Pull your last set of invoices, payment records, processor statements, proposal templates, and contracts. Look at what happened, not what you think happened. Where are clients getting confused? Which payment methods are expensive? How often are invoices delayed internally before they even reach the client? How many exceptions has your team normalized?

Audit these areas first:

- Payment methods in use: Card, ACH, wire, check, portal billing, international transfers.

- Invoice timing: Whether billing happens on schedule or after project staff chase details.

- Approval friction: Which clients require extra paperwork, backup, or purchase order references.

- Contract mismatch: Where signed terms don't line up with the billing cadence your team follows.

- System sprawl: Every spreadsheet, inbox, or manual workaround keeping the process alive.

You don't need perfection at this stage. You need a truthful map.

Phase two set strategy and choose tools

Once the problems are visible, define what success looks like. Faster collections. Cleaner project billing. Better margin retention. Less administrative overhead. More predictable cash flow. Pick the few outcomes that matter most.

Then choose the stack. For many firms, that means some combination of QuickBooks for accounting, Stripe for online payments, and a proposal or project platform that can trigger billing events. For others, a bank treasury setup, ACH workflow, or specialized consultant will make more sense.

Decision filter: Choose the system your team will actually use under deadline pressure, not the one that looks impressive in a demo.

At this stage, set policy too. Decide when deposits are required. Decide which invoices can be paid by card. Decide how international clients are billed. Decide who owns follow-up.

Phase three integrate and train

Implementation fails when firms treat it as software setup instead of operational change.

Map the workflow from signed proposal to final payment. Build invoice templates. Standardize line items. Connect your processor to accounting. Set roles for project managers, operations, and finance. Create reminder sequences and escalation paths.

Then train the team on the process they should follow when things go wrong. Late approval. Partial payment. Client asks to split invoices. Change order appears mid-phase. Refund request. A strong system handles exceptions without forcing the founder into every decision.

A practical rollout sequence works best:

- Pilot one client type first. Start with a repeatable engagement.

- Refine invoice language. Remove ambiguity before scaling.

- Test internal handoffs. PM to finance is usually where details get lost.

- Launch with documented rules. Don't rely on verbal instructions.

- Review after the first billing cycle. Fix friction while it's fresh.

Phase four optimize continuously

Once the system is live, use it. Don't let it turn into another piece of software your team ignores.

Review payment timing, client behavior, disputes, and manual interventions. If certain invoice formats get approved faster, standardize them. If one payment method creates confusion, limit it. If retainers work better than ad hoc billing for a service line, repackage the offer.

Ongoing review also helps when you're preparing for financing, expansion, or leadership transitions. Clean financial operations create confidence. Lenders want predictable collections. Senior hires want stability. Buyers and partners want proof that the business isn't held together by founder memory.

Financial maturity doesn't happen when you install a platform. It happens when your firm can collect money cleanly, repeatedly, and without operational drama.

How to Choose Your Merchant Advisory Partner

Most firms make this decision backwards. They choose a processor first, then try to force their billing reality into the tool. That's how you end up with awkward workarounds, confused clients, and hidden cost.

Choose the partner based on your business model. An architecture firm with phased billing has different needs than an interior design studio managing product purchases. A branding agency with global clients has different risks than a local residential practice.

The main partner categories

You generally have three choices. Traditional banks, all-in-one fintech platforms, and specialized advisors or boutique consultants.

Banks can be solid for treasury services, ACH, and account stability. They often move slower and may not understand project-based creative workflows. Fintech platforms are faster and easier to deploy. They can be excellent if your team needs user-friendly payment links, automated reminders, and straightforward integrations. Specialized advisors bring the most strategic value when your billing model is complex and your internal process is messy.

What to evaluate before you sign

Use a hard checklist. If a provider can't answer these questions clearly, move on.

- Project-based fit: Can they support deposits, milestone billing, retainers, and reimbursable expenses without awkward manual work?

- Fee transparency: Do you understand the total cost by payment type, not just the headline rate?

- Accounting integration: Will this connect cleanly to QuickBooks and your current reporting process?

- Client experience: Is the payment path simple for procurement teams, not just friendly for your bookkeeper?

- International capability: Can they handle multi-currency invoicing or cross-border payments with less friction?

- Support quality: When a large payment gets stuck, do you get real help or generic ticketing?

- Scalability: Will this still work when your project volume and average invoice size increase?

The cheapest option often becomes the most expensive once your team starts spending hours fixing what the platform can't handle.

Merchant Advisor Partner Comparison

| Partner Type | Best For | Fee Structure | Design Industry Expertise |

|---|---|---|---|

| Traditional bank | Firms prioritizing account stability, treasury controls, and ACH workflows | Often more negotiated and relationship-based, but can be less transparent in day-to-day use | Usually low unless you work with a banker who knows project-based services |

| All-in-one fintech platform | Firms that need speed, online invoicing, payment links, and easy integration | Usually clear at the platform level, but costs can rise if you overuse premium payment methods | Moderate, depending on how adaptable the platform is to retainers and milestone billing |

| Specialized advisor or boutique consultant | Firms with complex billing models, high-touch clients, or multi-system friction | Advisory fees vary, but the value comes from process design and cost control | Highest when the advisor has real experience with service businesses and creative operations |

Red flags to avoid

Some warning signs are easy to miss in sales conversations:

- They only talk about rates. That's not advisory. That's a commodity pitch.

- They don't ask about contracts. Then they don't understand collections.

- They ignore your team workflow. A tool that finance likes but PMs avoid will fail.

- They can't explain exceptions. Real firms deal with split billing, revisions, and disputed scopes.

- They oversell automation. Automation works only after the underlying process is disciplined.

A good partner should make your firm more predictable, not more dependent on hacks.

Merchant Advisory in Action Real World Scenarios

Theory matters less than operational reality. Here are three situations that come up constantly in growing design firms, and how merchant advisory changes the outcome.

The architecture firm with milestone confusion

A mid-sized architecture practice wins larger commercial work. Great news. The problem is that billing language in proposals doesn't match the actual project sequence. The team invoices late because PMs are waiting for final internal confirmation. Clients approve slowly because line items are vague.

An advisor fixes the structure. Billing milestones get tied to clear project phases. Invoices include the right documentation. Payment methods are narrowed so clients use the path that fits larger balances. The result isn't magical. It's disciplined. Collections become more predictable, and leadership can forecast staffing with less guesswork.

The product design and development market is projected to grow at a CAGR of 10.08% through 2030, with a pivot toward verification and validation services, according to Grand View Research's product design and development services analysis. Firms that price and bill complex work properly will be in a stronger position to capture that demand.

The interior design studio buried in pass-through spending

An interior design founder has a healthy book of business but constant cash strain. Client retainers, procurement payments, service fees, and vendor purchases are all flowing through a system that wasn't designed to separate them well. Every reconciliation cycle becomes detective work.

The fix starts with segmentation. Service fees get billed distinctly from reimbursable product costs. Approval paths are documented. Client-facing invoices become easier to read. The studio also sets firmer rules around when procurement begins and what must be funded in advance.

The financial improvement here isn't just operational. It also changes how the firm presents itself. Clients see a more professional process, which supports trust and smoother approvals. That same clarity is useful in public-facing channels too, especially when firms are trying to strengthen positioning through better visual marketing, as discussed in this piece on boosting architecture social media engagement.

The branding agency with international billing friction

A branding agency signs clients in multiple countries. Creative work is strong. Billing is clumsy. Some clients prefer card, some want bank transfer, some need invoices in local currency conventions. The agency spends too much time translating payment logistics instead of doing the work.

An advisor helps standardize the client payment experience. The agency creates approved billing paths, aligns contract language to cross-border realities, and reduces reliance on one-off manual instructions. Internal bookkeeping improves because records are cleaner and exceptions are fewer.

Complex creative work deserves a payment system that feels as intentional as the work itself.

Different firm types need different setups. That's the whole point. Merchant advisory isn't valuable because it's financial. It's valuable because it adapts financial operations to the way design businesses deliver services.

Key Metrics and Common Pitfalls to Avoid

If you don't measure the system, you won't improve it. You also won't know whether your advisor, platform, or revised billing policy is helping or just giving everyone new dashboards to stare at.

Metrics worth tracking every month

You don't need a giant finance department to monitor the right signals. You need a short list that informs decisions.

- Effective processing rate: What you're really paying across all accepted payment types.

- Days sales outstanding: How long it takes to collect after invoicing.

- Invoice aging by client: Which accounts are becoming a pattern, not a one-off issue.

- Administrative time spent on billing: Whether your team is still doing avoidable manual work.

- Exception volume: Split payments, disputed line items, manual corrections, and payment rerouting.

- Collection by service line: Which offers are easy to bill and which ones create friction.

- Write-offs and concessions: The money lost because your process wasn't tight enough.

These metrics matter because they reveal process quality. A firm that looks busy can still be leaking margin through unnecessary admin time, delayed invoicing, poor payment method control, or weak follow-up.

Common mistakes that keep firms stuck

The first mistake is chasing the lowest fee. That's shallow thinking. If the cheaper solution creates more admin work, poorer reporting, or a frustrating client experience, your real cost goes up.

The second mistake is ignoring the client payment experience. Design firms care a great deal about presentation in every other part of the business. Then they send confusing invoices with unclear backup and awkward payment instructions. That mismatch hurts trust.

A third mistake is choosing a system that can't scale. It may work for a founder and an office manager. It won't work when project managers, finance staff, and outside consultants all need visibility. Process maturity has to grow with client expectations.

Another common problem is failing to align financial clarity with visual clarity. Clients interpret your professionalism through every touchpoint, including proposals, invoices, deliverables, and brand presentation. The same issue often shows up in project communication, where mismatched expectations create avoidable friction, a challenge explored in this article on managing client visual expectations.

Watch for this: When your team says, "That's just how this client pays," they're often describing a process failure you've accepted as normal.

The discipline that matters

Most payment problems in design firms aren't dramatic. They're repetitive. Slightly late invoices. Slightly unclear approvals. Slightly inconsistent terms. Those small defects add up.

Good merchant advisory doesn't just install a platform. It gives leadership the habit of reviewing the right metrics, fixing recurring friction, and refusing to let "temporary" workarounds become permanent operating procedure.

Build Your Firm on a Foundation of Financial Clarity

Growing design firms don't fail because the work lacks quality. They stumble because operational complexity outruns financial discipline.

That's why Merchant Advisory for Growing Design Firms matters. It gives founders a way to treat payments, billing, and cash flow as strategic infrastructure. Not admin. Not cleanup work. Infrastructure. The kind that supports larger projects, better client experience, stronger margin protection, and calmer decision-making.

If your firm is still relying on manual invoicing, inconsistent terms, unclear payment rules, or founder memory to keep collections moving, fix that now. Waiting doesn't make the problem smaller. It makes the next stage of growth harder.

Start with one move. Audit your current setup. Review how you invoice, how clients pay, where delays happen, and where margin disappears. Then tighten the system in stages. Better payment methods. Better contracts. Better workflow. Better reporting.

The firms that scale cleanly are rarely the firms with the most chaotic hustle. They're the firms with enough operational maturity to support their ambition.

That can be your firm. But only if your financial systems grow up with the rest of the business.

If your architecture or design firm also needs images that support premium positioning, Jimmy Clemmons Photographer creates architectural imagery, commercial brand content, and professional portraits that help design-driven businesses present their work with clarity and authority. Strong operations help you get paid. Strong visuals help clients understand why you're worth it.